AI For Humanity

Lecture 11 - Double ML

2025-11-19

Econometrics and AI

- Econometrics 1, 2 and Applied Policy Evaluation

- Focus is on regression

- Regression is cool! Gift that keeps on giving

- But what about using AI with econometrics?

- Let’s first take a little detour/recap on regression to see where we are coming from

- I have picked out some highlights from (Angrist & Pischke, 2008) in the following

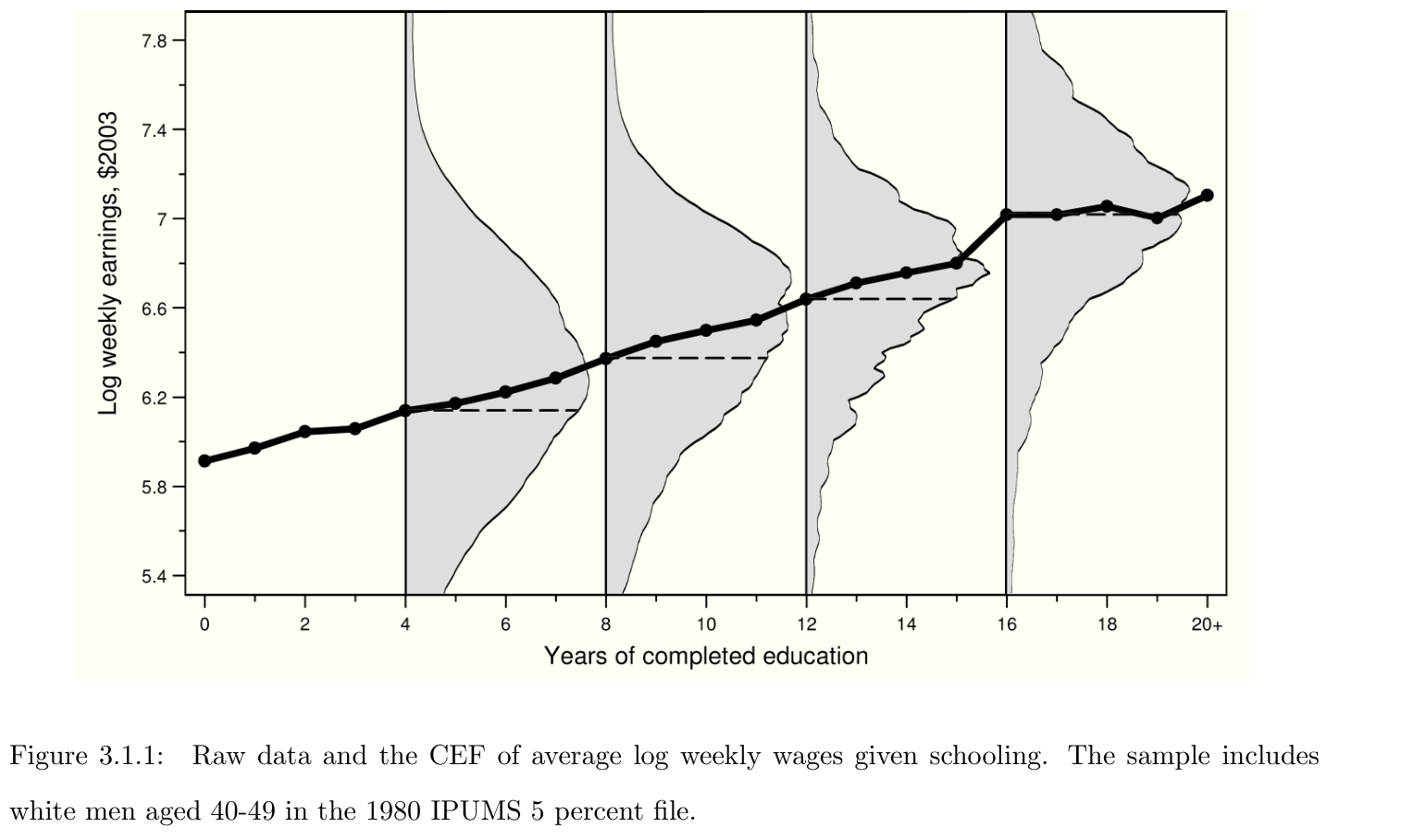

Econometrics and Regression

CEF Decomposition property: for \(Y\) an outcome variable and \(X\) a \(k \times 1\) vector of covariates, we have the decomposition: \[\begin{align} \label{eq:cefdecomp} Y = E[Y \mid X] + \varepsilon \end{align}\] where \(E[Y \mid X]\) is the conditional expectation function (CEF) and

- \(\varepsilon\) is mean-independent of \(X\) i.e. \(E[\varepsilon \mid X] = 0\)

- \(\varepsilon\) is uncorrelated with any function of \(X\)

Econometrics and Regression

Let \(m(X)\) be any function of \(X\). The CEF solves:

\[\begin{align*} E[Y \mid X] = \underset{m(X)}{\arg\min} \ E \left[ \{Y - m(X)\}^{2} \right] \end{align*}\]

i.e. it is the minimum mean squared error (MMSE) predictor of \(Y\) given \(X\).

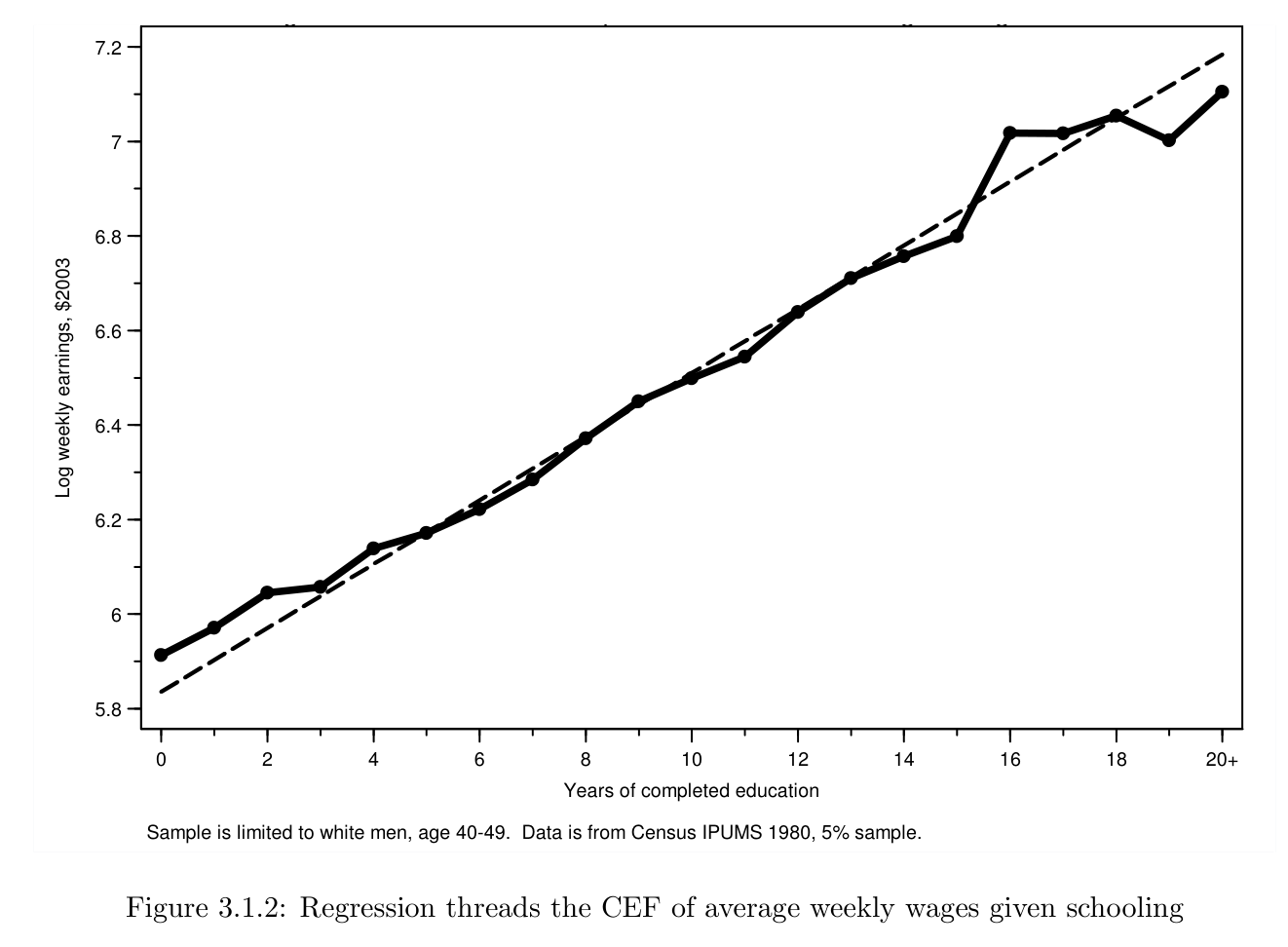

Regression estimand

Regression estimates provide a valuable baseline for almost all empirical research because regression is tightly linked to the CEF, and the CEF provides a natural summary of empirical relationships.

- 3 ways Angrist & Pischke motivates regression as our primary tool

- \(\beta\): vector of population regression coefficients, defined as the solution to a population least squares problem: \[\begin{align} \label{eq:argminbeta} \beta = \underset{b}{\arg\min} \ E \left[ (Y - X'b)^{2} \right] \end{align}\] First-order condition (FOC): \[\begin{align} \label{eq:beta} E \left[ X(Y - X'\beta) \right] = 0 \iff \beta = E[XX']^{-1}E[XY]. \end{align}\]

- \(\beta_{k} = \mathrm{cov}(\tilde{X}_{k}, \tilde{Y})/\mathrm{Var}(\tilde{X}_{k})\); FWL; ceteris paribus; \(E \left[ Xe \right] = 0\), \(e := Y - X'\beta\)

Regression Justifications

- Linear CEF Theorem: Suppose the CEF is linear. Then the population regression function is it.

- Assume \(E[Y \mid X] = X'\beta^{*}\); insert in FOC and solve

- The Best Linear Predictor Theorem: The function \(X'\beta\) is the best linear predictor of \(Y\) given \(X\) in a MMSE sense.

- \(\beta = E[XX']^{-1}E[XY]\) solves the population least-squares problem

- The Regression-CEF Theorem: The function \(X'\beta\) provides the MMSE linear approximation to \(E[Y \mid X]\) i.e. \[\begin{align}

\label{eq:cefapprox}

\beta = \underset{b}{\arg\min} \, E \left\{ (E[Y \mid X] - X'b)^{2}

\right\}.

\end{align}\]

- Apply the LIE to the FOC to see \(E \left[ X(Y - X'\beta) \right] = 0 \iff E \left[ X(E[Y \mid X] - X'\beta) \right] = 0\)

CEF and Regression-CEF Theorem

Regression Justifications

- The regression-CEF theorem is Angrist & Pischke’s favorite way to motivate regression

The statement, that regression approximates the CEF, lines up with our view of empirical work as an effort to describe the essential features of statistical relationships, without necessarily trying to pin them down exactly

- This is cool!

- But what if:

- CEF, \(E[Y \mid X]\), is high-dimensional and non-linear?

- Regression provides the best MMSE linear approximation to \(E[Y \mid X]\), but this might not be good enough in more complex (high-dimensional + non-linear) scenarios

- Can we use machine learning to estimate the CEF and conduct valid inference on some target parameter of interest (that depends on estimating the CEF in a first step)?

Statistical modelling in the age of data science

- Breiman’s two worlds

- Tradition within:

- Computer science: let the data speak by making use of flexible, black-box predictive models

- Focus on prediction

- No statistical inference

- Statistics/econometrics: use (semi)parametric models with the primary aim to provide insight into data

- Focus more on the model than on the problem one is trying to solve

- Great danger in drawing false conclusions when viewing the fitted model as a representation of the ground truth

- Computer science: let the data speak by making use of flexible, black-box predictive models

Statistical modelling in the age of data science

- Bridging the two cultures

- Rapidly growing interest within causal inference literature in leveraging data-adaptive methods for inferring effects of treatments on outcomes

- Data-adaptive:

- Uses the data to learn structure and can be automated such that it can be pre-specified without ambiguity

- Random forest, gradient boosting, etc.

- How is it done in practice?

Choosing an estimand

- Starting point of analysis: not the choice of a model, but the choice of an estimand

- An estimand represents an interpretable summary that we wish to target in our analysis

- Connected to main scientific/research question of interest

- Defined in a model-free way; can be unambiguously specified before seeing the data

- Example: average treatment effect (ATE), which can be identified under causal assumptions as: \[\begin{align*}

\theta_{0} = E[Y(1) - Y(0)]

= E\{

E[Y\mid D = 1, X]

- E[Y\mid D = 0, X]

\}.

\end{align*}\] where

- \(\theta_{0}\) estimand/target parameter

- \(E[Y\mid D = 1, X]\) and \(E[Y\mid D = 0, X]\) nuisance parameters

Angrist & Pischke - Estimands

Two quotes:

Our “population first” approach to econometrics is motivated by the fact that we must define the objects of interest before we can use data to study them.

(Angrist & Pischke 2008, p 23) [boldface mine]

… it’s kosher — even desirable — to think about what a set of population parameters might mean, without initially worrying about how to estimate them.

(Angrist & Pischke 2008, p 28)

Estimation

After having chosen an estimand and done identification comes estimation

Estimation is done with an estimator

One estimator for the ATE is: \[\begin{align*} \frac{1}{n}\sum_{i=1}^{n} \{\hat{E}[Y_{i} \mid D_{i} = 1, X_{i}] - \hat{E}[Y_{i} \mid D_{i} = 0, X_{i}]\} \end{align*}\] where the components are trained machine learning algorithms for the outcome in treated and non-treated units

Applying the estimator to a concrete dataset yields a number called the estimate

Problems with naive approach

- Estimator on previous slide typically poor

- ML algorithms tuned for prediction, not for estimating association measures

- Estimator sensitive to estimation error in the ML components

- Double machine learning (DML) is one framework to construct estimators that are non-sensitive to estimation error in the nuisances

- With DML:

- More time can be spent on translating scientific questions into interpretable estimands (that may or may not be linked to a statistical model)

- Less time spent on interpreting wrong model

DML

- DML: Double/debiased machine learning

- A general approach to performing inference about a target parameter (estimand) in the presence of (high-dimensional) nuisance parameters

- Using machine learners as nuisance estimators leads to biases:

- Regularization bias

- Overfitting bias

- DML:

- reduces the impact of nuisance parameter estimation on estimators of the parameter of interest

- assumption-lean modeling; accommodates use of complex data types, e.g. text data

- Two essential components:

- Neyman orthogonality

- Cross-fitting

DML estimator

A DML estimator is a plug-in estimator that leverages a first-step nuisance parameter estimator by relying on Neyman orthogonal scores and cross-fitting

- It is DML’s combination of Neyman orthogonality and cross-fitting that allows for valid statistical inference on the target parameter

- Stress on combination: doesn’t work with only one of them

- We’ll return to that

DML setup

- \(W = (Y, D, X)\) tuple of data for \(Y\) outcome, \(D\) treatment and \(X\) covariates

- User-specified target parameter \(\theta_0\) defined as the solution to a moment condition: \[\begin{align}

\label{eq:moment-condition}

E \left[ m(W, \theta_{0}, \eta_{0}) \right] = 0

\end{align}\] where

- \(m(W, \theta, \eta)\) is a known (possibly vector-valued) user-specified score function indexed by \(\theta \in \Theta\)

- \(\eta_{0} \in \mathcal{T}\) is a nuisance parameter, which is not of direct interest but is needed for estimating \(\theta_{0}\)

- Parameter is a general concept here; \(\eta_0\) is often a collection of functions to be estimated with machine learners

- \(\Theta\) is a low-dimensional parameter space, while \(\mathcal{T}\) is a possibly high-dimensional parameter space

Score function for the ATE

- Average treatment effect (ATE) as our target parameter: \[\begin{align*} \theta_{0} = E[Y(1) - Y(0)] = E\{ E[Y\mid D = 1, X] - E[Y\mid D = 0, X] \}, \end{align*}\] identified by the regression adjustment estimand (RHS) under conditional exogeneity

- Score \[\begin{align*} m(W; \theta_{0}, \eta_{0}) &= E[Y\mid D = 1, X] - E[Y\mid D = 0, X] - \theta_{0} \\ &= \ell_{0}(1, X) - \ell_{0}(0, X) - \theta_{0} \end{align*}\] where \(\ell_{0}(D, X) := E[Y \mid D, X]\); here, \(\eta_0 = \ell_0\) is the nuisance parameter (function)

- Notice: \[\begin{align*} E \left[ m(W; \theta_{0}, \eta_{0}) \right] = 0 & \iff E \left[ E[Y\mid D = 1, X] - E[Y\mid D = 0, X] - \theta_{0} \right] = 0 \\ & \iff \theta_{0} = E \left[ E[Y\mid D = 1, X] - E[Y\mid D = 0, X] \right] \end{align*}\] i.e. the score identifies our target parameter, the ATE

Two other scores

Two other scores that identify the ATE:

- Inverse propensity weighted (IPW) score: \[\begin{align*} m(W_{i}; \theta, \eta) = \alpha(D_{i}, X_{i})Y_{i} - \theta \end{align*}\] where \[\begin{align*} \alpha_{0}(D_{i}, X_{i}) = \frac{D_{i}}{r_{0}(X_{i})} - \frac{1 - D_{i}}{1 - r_{0}(X_{i})}, \quad r_{0}(X_{i}) = E[D_{i} \mid X_{i}] = P(D_i = 1 \mid X_i), \end{align*}\] and \(\eta = \alpha\).

- Doubly robust score: \[\begin{align} \psi(W_{i}; \theta_{0}, \eta) = \alpha(D_{i}, X_{i})[Y_{i} - \ell(D_{i}, X_{i})] + \ell(1, X_{i}) - \ell(0, X_{i}) - \theta_{0} \end{align}\] where \(\eta = (\alpha, \ell)\)

Plug-in estimators

- Plug-in estimators can be constructed as roots to the sample average of the scores: \[\begin{align} \label{eq:root-plugin} \frac{1}{n} \sum_{i=1}^{n} m(W_{i}; \check{\theta}, \check{\eta}) = 0 \end{align} \tag{1}\]

- In practice:

- estimate nuisance \(\eta_0\) with estimator \(\check{\eta}\)

- plug it into sample moment condition and solve for estimator of target parameter

- Regression adjustment example: \[\begin{align} \frac{1}{n} \sum_{i=1}^{n} m(W_{i}; \check{\theta}, \check{\eta}) = 0 \iff \check{\theta} = \frac{1}{n}\sum_{i=1}^{n} \left[ \hat{\ell}(1, X_{i}) - \hat{\ell}(0, X_{i}) \right] \end{align}\] where \(\hat{\ell}(1, X_{i})\) estimator of \(E[Y \mid D = 1, X]\) trained on subset with \(D = 1\) and \(\hat{\ell}(0, X_{i})\) estimator trained on subset with \(D = 0\)

Score Taylor expansion

- Using Equation 1 and a first-order Taylor expansion we get: \[\begin{align*} 0 = \frac{1}{n} \sum_{i=1}^{n} m(W_{i}; \check{\theta}, \check{\eta}) &\approx \frac{1}{n} \sum_{i=1}^{n} m(W_{i}; \theta_{0}, \eta_{0}) \\ & \quad +\; \frac{1}{n} \sum_{i=1}^{n} \frac{\partial}{\partial \theta} m(W_{i}; \theta_{0}, \eta_{0})(\check{\theta} - \theta_{0}) \\ &\quad +\; \frac{1}{n} \sum_{i=1}^{n} \frac{\partial}{\partial \eta} m(W_{i}; \theta_{0}, \eta_{0})(\check{\eta} - \eta_{0}) \\ \iff \label{eq:decomp} \sqrt{n}(\check{\theta} - \theta_{0}) &\approx \left[ -\frac{1}{n}\sum_{i=1}^{n} \frac{\partial}{\partial \theta} m(W_{i}; \theta_{0}, \eta_{0}) \right]^{-1} \frac{1}{\sqrt{n}} \sum_{i=1}^{n} m(W_{i}; \theta_{0}, \eta_{0}) \\ & + \left[ -\frac{1}{n}\sum_{i=1}^{n} \frac{\partial}{\partial \theta} m(W_{i}; \theta_{0}, \eta_{0}) \right]^{-1} \frac{1}{\sqrt{n}} \sum_{i=1}^{n} \frac{\partial}{\partial \eta} m(W_{i}; \theta_{0}, \eta_{0})(\check{\eta} - \eta_{0}) \end{align*}\]

Taylor expansion of score - comments

- Focus is on case where:

- We have as many score equations as parameters of interest (to be able to invert the matrix \(\left[ -\frac{1}{n}\sum_{i=1}^{n} \frac{\partial}{\partial \theta} m(W_{i}; \theta_{0}, \eta_{0}) \right]^{-1}\))

- A sample root exists

- First-order dependence of \(\check{\theta}\) and \(\check{\eta}\) poses substantial complications in settings where the nuisance parameter is high-dimensional

- Here, \(\check{\eta}\) corresponds to a flexible estimator

- Complication results because flexible estimators are often associated with non-negligible bias and variance.

- The corresponding expansion in a high-dimensional setting may be dominated by the final term that involves \(\check{\eta}\).

Two sources of biases

- Term corresponding to estimation error in \(\eta_{0}\) of expansion: \[\begin{align*} \frac{1}{\sqrt{n}} \sum_{i=1}^{n} \frac{\partial}{\partial \eta} m(W_{i}; \theta_{0}, \eta_{0})(\check{\eta} - \eta_{0}) \end{align*}\]

- The dominance of this term generally implies two distinct sources of bias in the target parameter estimator \(\check{\theta}\):

- Regularization bias

- Overfitting bias

- Regularization bias arises because the estimation error \(\check{\eta} - \eta_{0}\) is too large

- Overfitting bias appears because \(\check{\eta} - \eta_{0}\) is strongly correlated with \(W_{i}\)

- Both biases imply a failure of conventional statistical inference on our target parameter

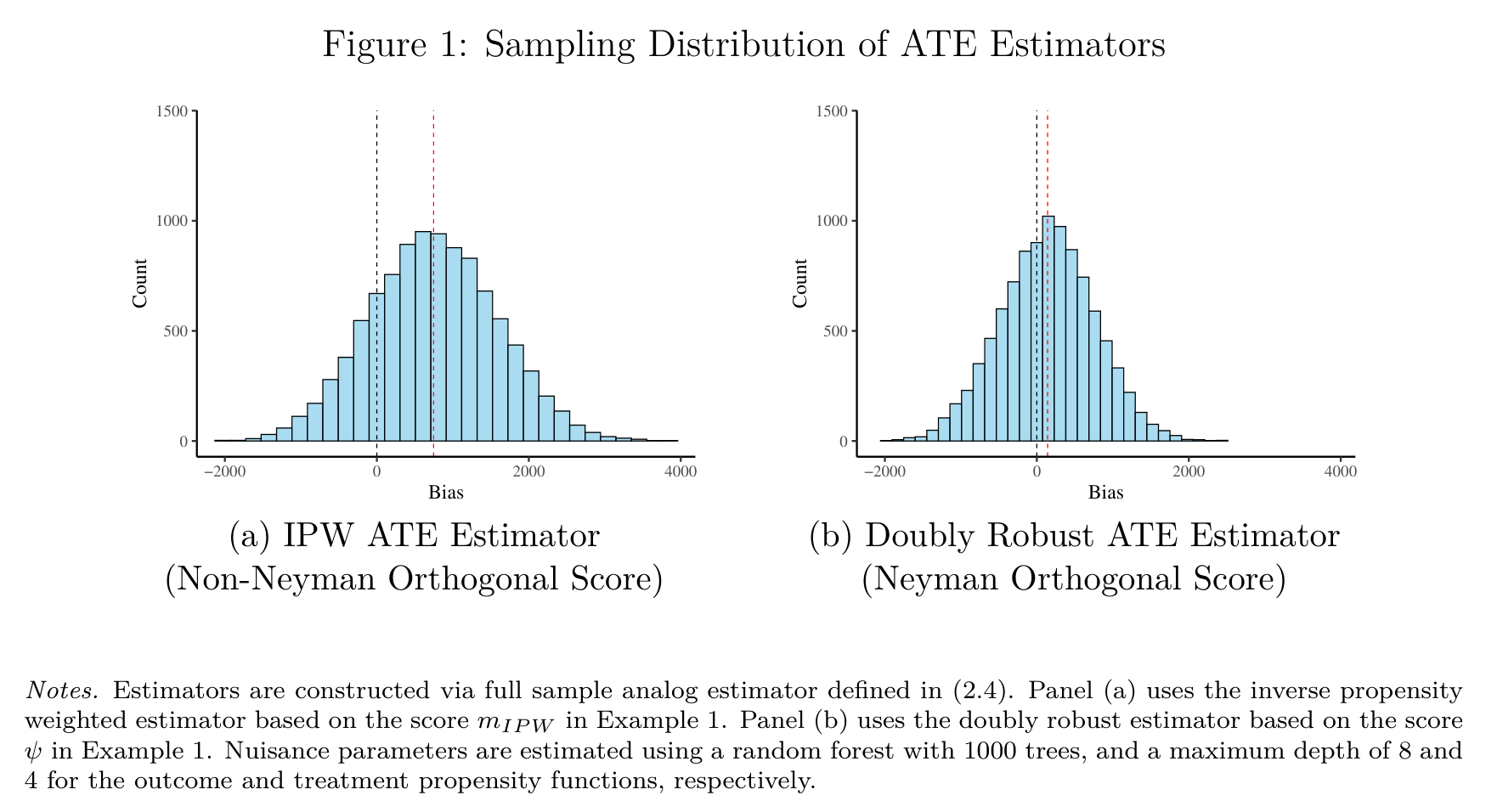

Neyman Orthogonality

- A Neyman orthogonal score is a score function \(\psi\) that satisfies \[\begin{align} E\left[ \psi(W_{i}; \theta_{0}, \eta_{0}) \right] & = 0, \\ \frac{\partial}{\partial \lambda} E\left[ \psi(W_{i}; \theta_{0}, \eta_{0} + \lambda [\eta - \eta_{0}]) \right] \Big|_{\lambda =0} & = 0, \quad \forall \eta \in \mathcal{T}, \end{align}\] where \(\eta\) and \(\lambda\) can be interpreted as the direction and magnitude of a deviation away from the true nuisance parameter \(\eta_{0}\), respectively

- The notation \(m\) is for an arbitrary score while \(\psi\) is for a Neyman orthogonal score

- Neyman orthogonality:

- Is a local robustness property of the score function that decreases sensitivity of the score the resulting plug-in estimator to the nuisance parameter

- Allieviates regularization bias

- Practical implication: inferential statements about \(\theta_{0}\) do not depend on the precise statistical properties of the nuisance estimator \(\check{\eta}\)

Neyman Orthogonality and bias term

- Estimation error in \(\eta_{0}\) of expansion now with Neyman orthogonal score \(\psi\)

- Neyman Orthogonality implies \(\frac{\partial}{\partial \eta} \psi(W_{i}; \theta_{0}, \eta_{0})\) is mean zero

- If the first-step estimation error \(\check{\eta} - \eta_{0}\) as also independent of data \(W_{i}\) then the bias term will vanish: \[\begin{align*} \frac{1}{\sqrt{n}} \sum_{i=1}^{n} \frac{\partial}{\partial \eta} \psi(W_{i}; \theta_{0}, \eta_{0})(\check{\eta} - \eta_{0}) = \sqrt{n}\left(\frac{1}{n} \sum_{i=1}^{n} \frac{\partial}{\partial \eta} \psi(W_{i}; \theta_{0}, \eta_{0})(\check{\eta} - \eta_{0}) \right) \approx 0 \end{align*}\] under mild convergence requirements on \(\check{\eta}\) and additional mild regularity conditions.

- As a consequence:

\[\begin{align*} \sqrt{n}(\check{\theta} - \theta_{0}) &\approx \left[ -\frac{1}{n}\sum_{i=1}^{n} \frac{\partial}{\partial \theta} m(W_{i}; \theta_{0}, \eta_{0}) \right]^{-1} \frac{1}{\sqrt{n}} \sum_{i=1}^{n} m(W_{i}; \theta_{0}, \eta_{0}) \end{align*}\]

Neyman Orthogonality Simulation

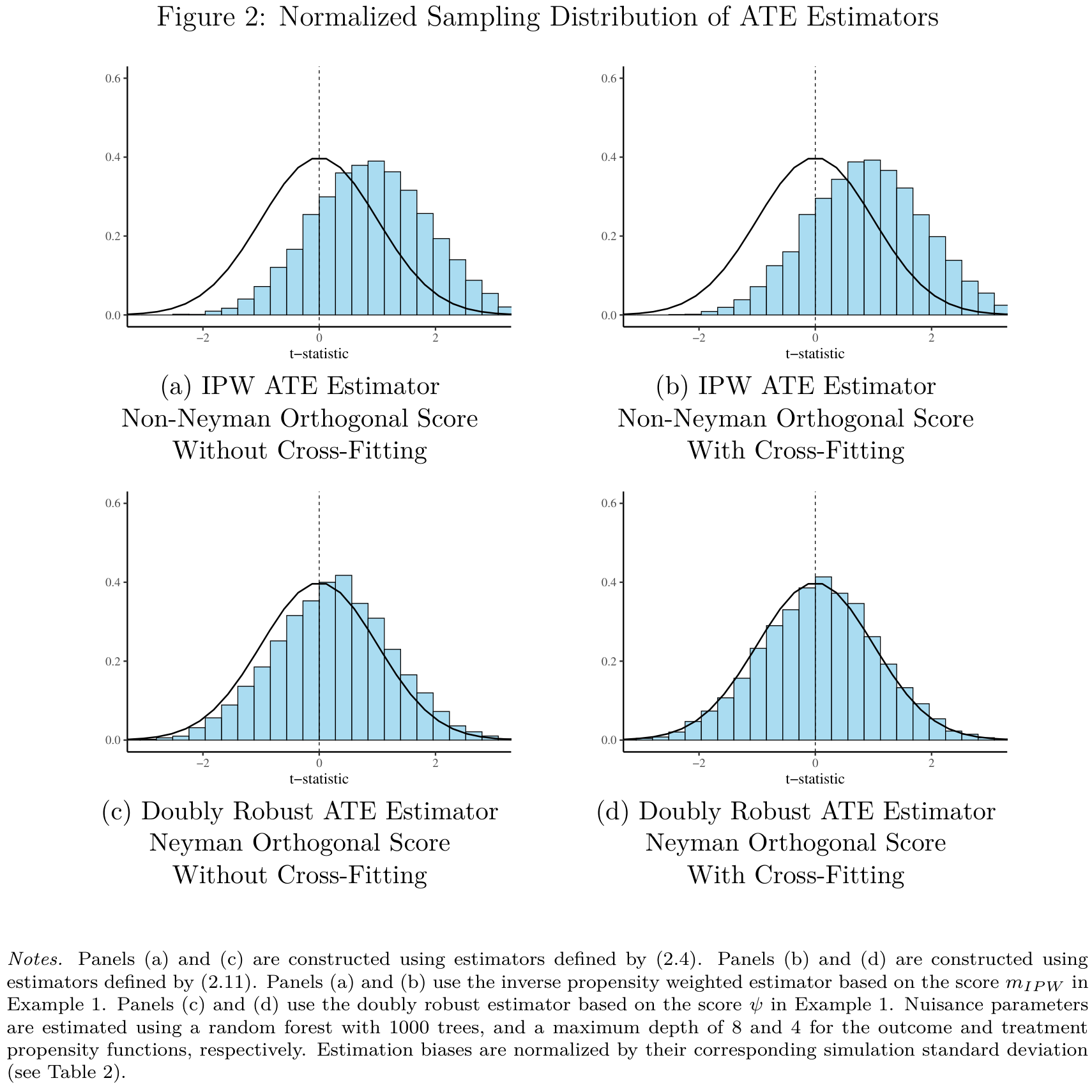

Cross-fitting

- In the expansion example, we assumed Neyman orthogonality and that the first-step estimation error \(\check{\eta} - \eta_{0}\) was independent of the data in order to get the bias term to vanish asymptotically

- Generally, Neyman orthogonality alone is not sufficient to guarantee that first-step estimation of nuisance parameters can be ignored in inference about low-dimensional target parameters

- This is where cross-fitting comes into play

- Cross-fitting is a form of repeated sample splitting intended to reduce dependence between first-step estimation error and the data, thus alleviating overfitting bias

Cross-fitted MM estimator

- Cross-fitted method of moments estimator: \[\begin{align}

\tilde{\theta}: \quad

\frac{1}{n} \sum_{k=1}^{K} \sum_{i \in I_{k}} m(W_{i};

\tilde{\theta}, \hat{\eta}_{-k}) = 0

\end{align}\] where

- \(\{I_{k}\}_{k=1}^{K}\) is a random partition of the sample of individuals \(\{1, \ldots, n\}\) into \(K\) subsamples of approximately equal size

- \(\{\hat{\eta}_{-k}\}_{k=1}^{K}\) are cross-fitted nuisance parameter estimators, each calculated on the observations excluding those in the sub-sample \(I_{k}\)

- Because \(\hat{\eta}_{-k}\) uses only observations not in sub-sample \(k\), the estimation error in \(\hat{\eta}_{-k}\) is independent of observations in sub-sample \(k\)

- This mechanically alleviates overfitting bias as long as observations are independent across \(i\)

Simulation

DML Estimator

- Now we can understand the definition:

A DML estimator is a plug-in estimator that leverages a first-step nuisance parameter estimator by relying on Neyman orthogonal scores and cross-fitting

- I.e. a DML estimator solves:

\[\begin{align} \label{eq:dml} \hat{\theta}: \quad \frac{1}{n} \sum_{k=1}^{K} \sum_{i \in I_{k}} \psi(W_{i}; \hat{\theta}, \hat{\eta}_{-k}) = 0 \end{align} \tag{2}\]

- Chernozhukov et al. (2018) provide conditions that allow researchers to make valid inferential statements about \(\theta_0\) using the DML estimator \(\hat{\theta}\)

- Besides sampling and regularity conditions, a central sufficient condition for DML to work is that the nuisance parameter estimator \(\hat{\eta}\) converges sufficiently fast

DML Asymptotic Distribution

- Under conditions on last line of prev. slide, the DML estimator is asymptotically normal \[\begin{align*} \sqrt{n}(\hat{\theta} - \theta_{0}) \overset{d}{\to} \mathcal{N}(0, \hat{\Sigma}), \end{align*}\] \[\begin{align*} \hat{\Sigma} & := \hat{J}^{-1} \left( \frac{1}{n} \sum_{k=1}^{K} \sum_{i \in I_{k}} \psi(W_{i}; \hat{\theta}, \hat{\eta}_{-k}) \psi(W_{i}; \hat{\theta}, \hat{\eta}_{-k})^{T} \right) \hat{J}^{-T} \\ \hat{J} & := \frac{1}{n} \sum_{k=1}^{K} \sum_{i \in I_{k}} \frac{\partial}{\partial \theta} \psi(W_{i}; \theta, \hat{\eta}_{-k}) \Big|_{\theta = \hat{\theta}} \end{align*}\]

- The \(1 - \alpha\) confidence intervals about the target parameter \(\theta_{0}\): \[\begin{align*} \left[ \hat{\theta} - c_{1 - \frac{\alpha}{2}} \cdot \sqrt{\mathrm{diag}(\hat{\Sigma})/n}, \hat{\theta} + c_{1 - \frac{\alpha}{2}} \cdot \sqrt{\mathrm{diag}(\hat{\Sigma})/n} \right] \end{align*}\]

- Practical implication: Neyman-orthogonal scores and cross-fitting leads to DML standard errors being the standard errors that would be used if the nuisance parameter estimates were taken as the true parameters.

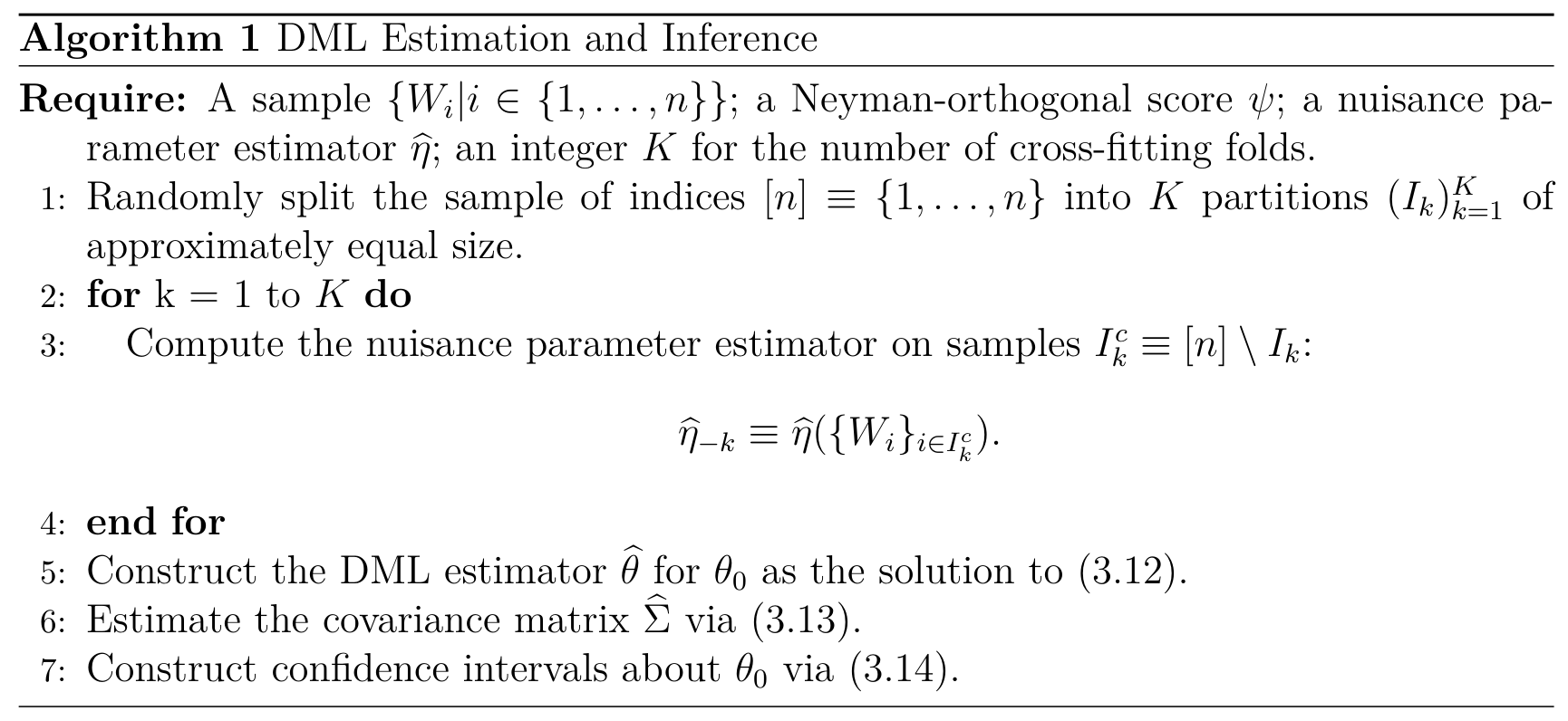

General DML Algorithm

- See estimator Equation 2 and standard errors

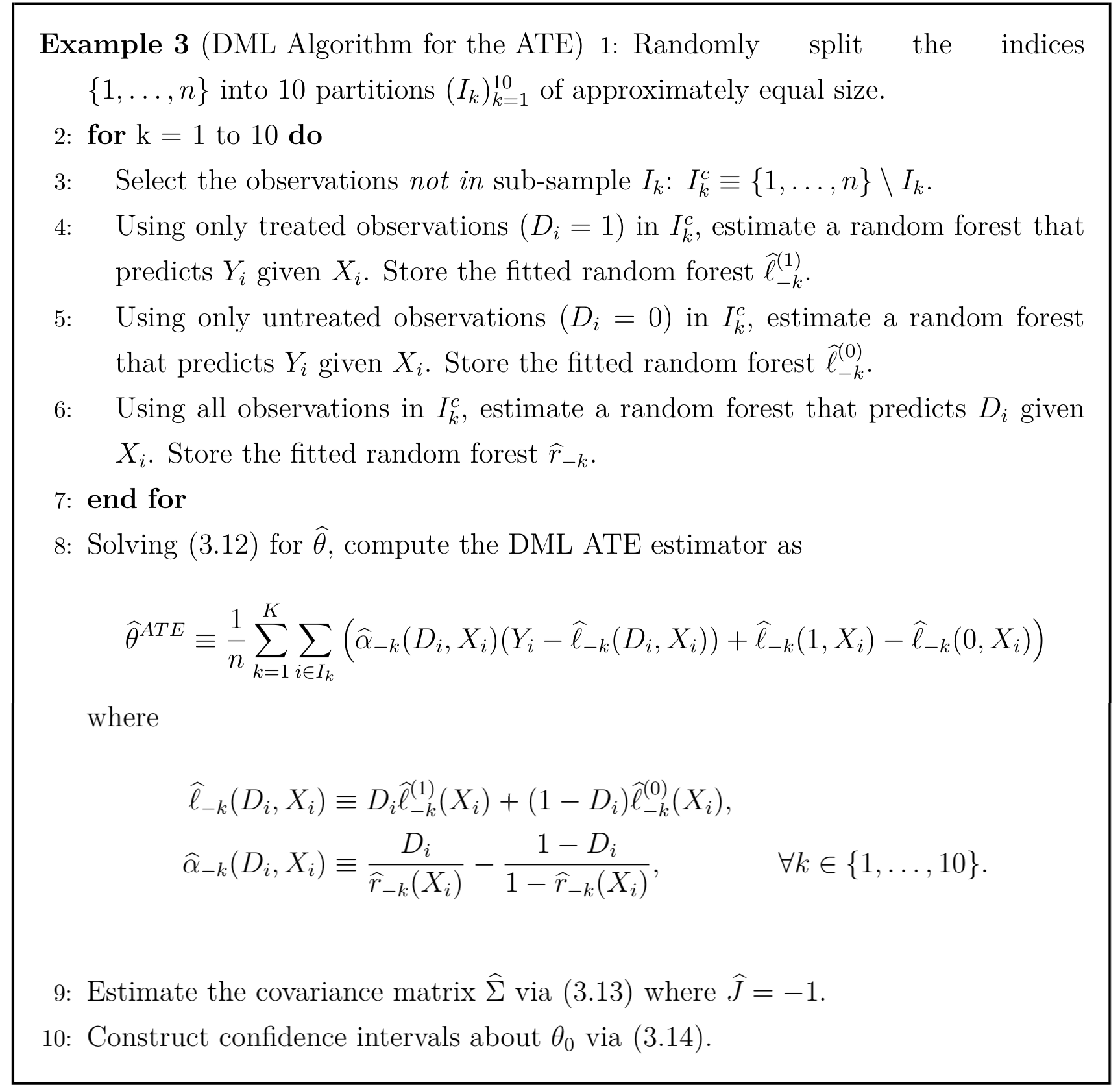

DML Algorithm ATE

Note: error in step 8. for \(\ell(D_{i}, X_{i})\) in the paper; should be a plus sign in the definition (this is corrected in the screenshot above)

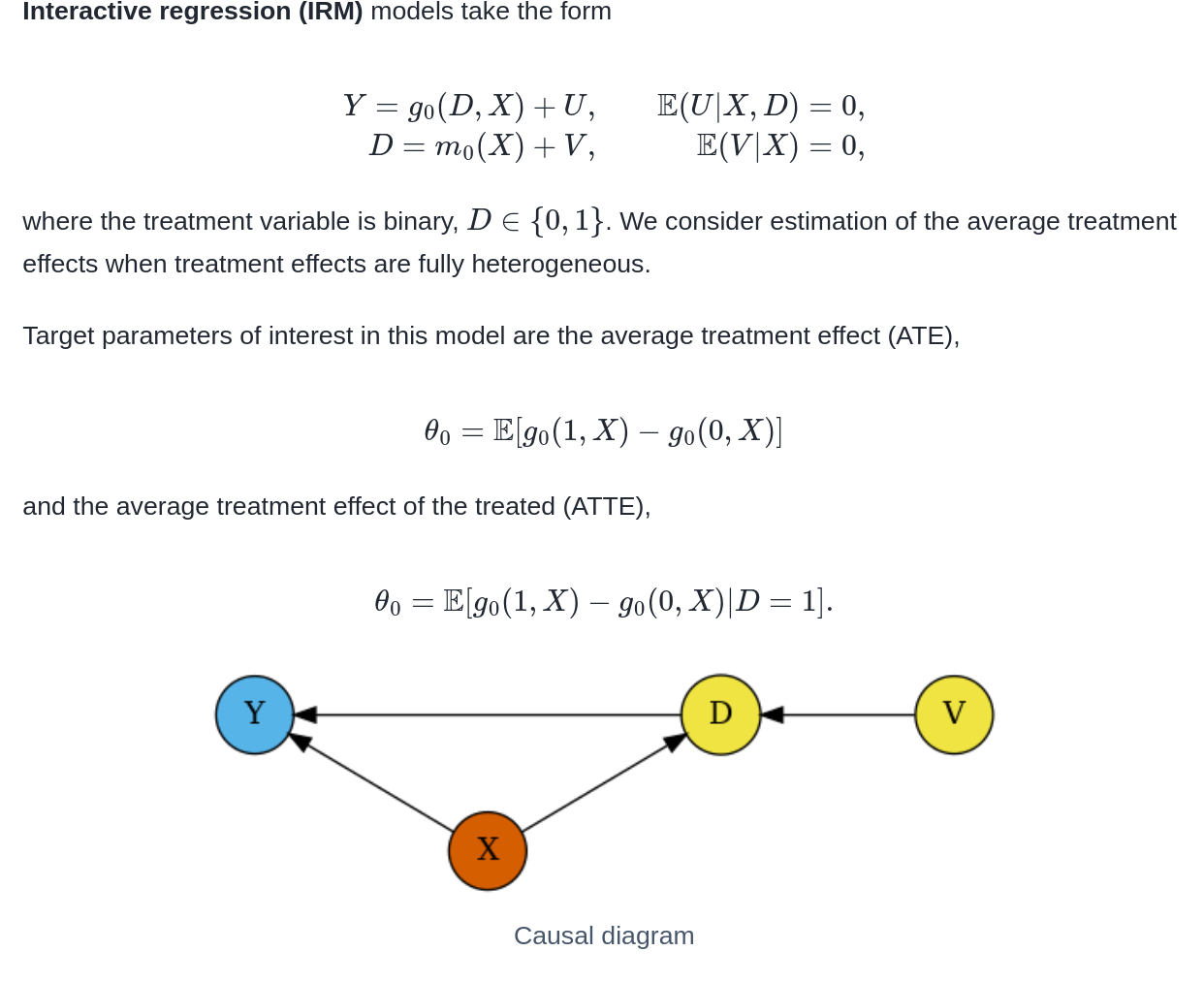

Example: DML pkg - IRM

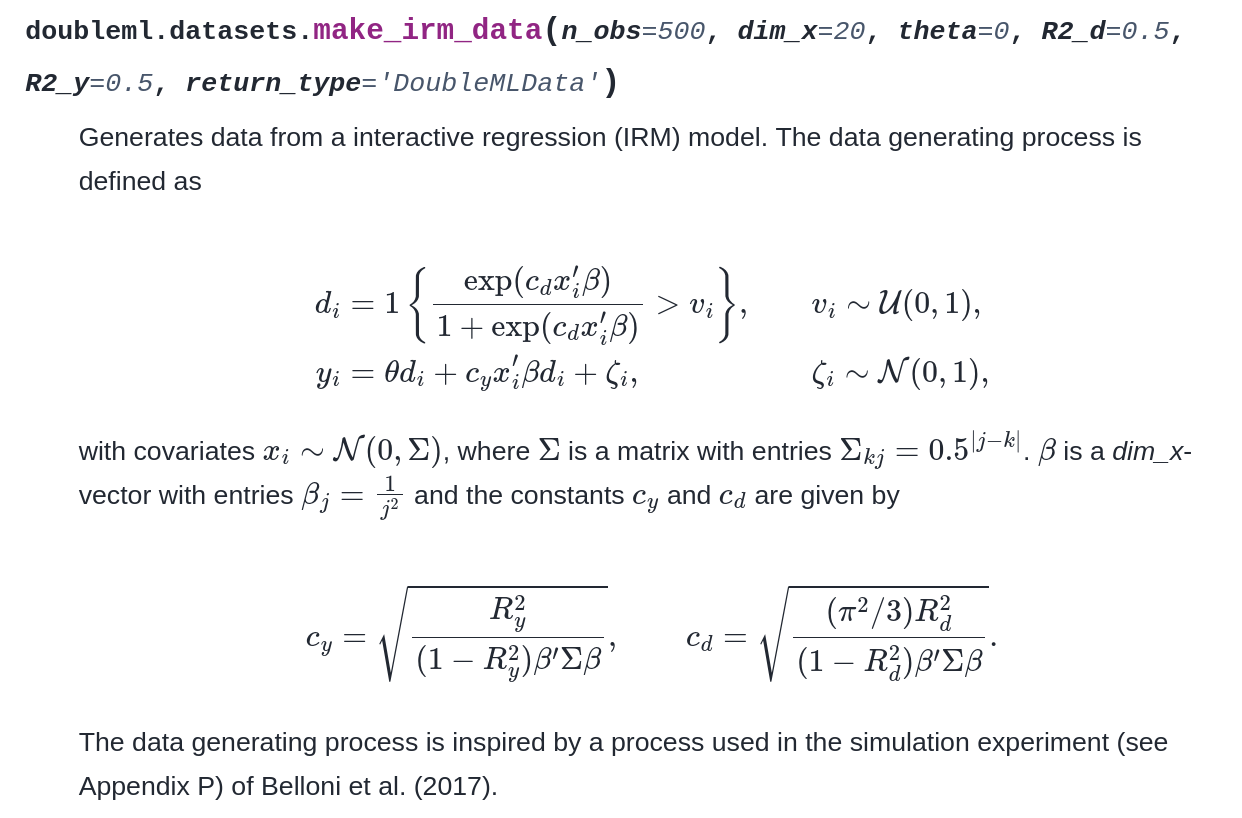

Example: DML pkg - DGP

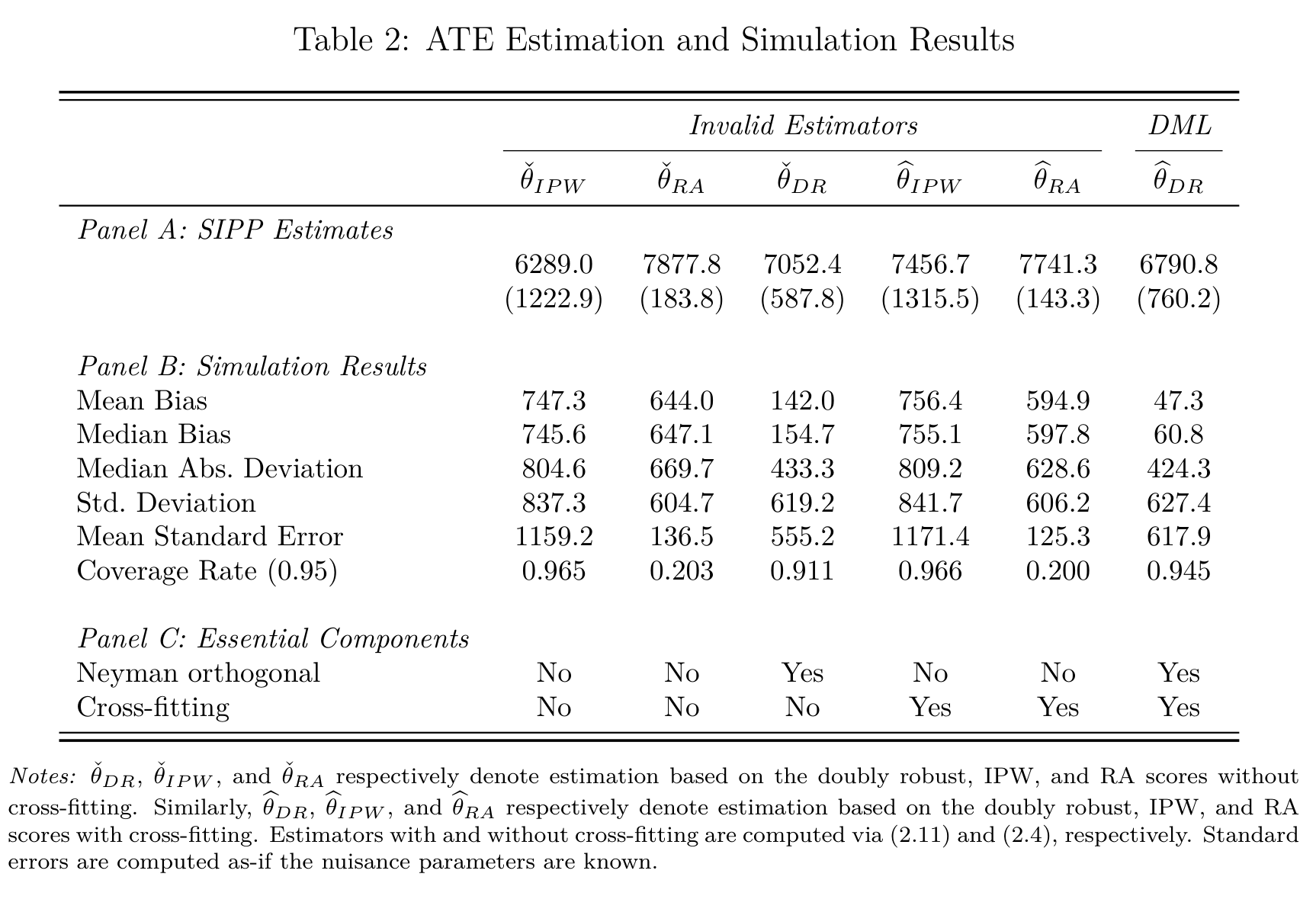

Example: 401K Eligibilty

- We focus on estimating the average effect of 401(k) eligibility, denoted by \(D\), on net financial assets, \(Y\)

- Estimand, ATE: \[\begin{align*} \theta_{0} = E[Y(1) - Y(0)] \end{align*}\]

- The key identification argument is that, conditional on observed demographics, 401(k) eligibility is as good as randomly assigned.

- Controls collected in vector \(X_i\) and we also assume overlap \(0 < P(D_{i} = 1 \mid X) < 1\)

- To estimate the ATE, consider the non-Neyman orthogonal IPW score, the Neyman orthogonal doubly robust score the regression adjustment (RA) score

- Nuisance estimators: random forests with 1000 trees and a maximum depth of 8 and 4 for the outcome and treatment propensity functions

Example: 401K Eligibilty results

True underlying ATE \(\approx 6889\)

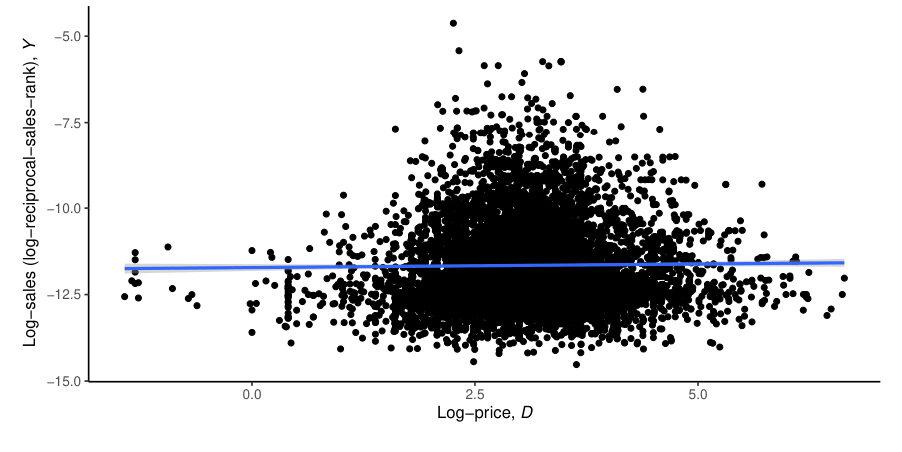

Example: price elasticity

Scientific question of interest:

What is the effect of setting a product’s price on the volume of its sales? I.e. what is its price elasticity of demand?

Scraped data on 9,212 toy cars from Amazon.com

\(D\) denotes the log of the price, \(Y\) the negative log of the sales rank (proxy for sales volume) of a toy car (randomly drawn from the population of toy cars sold on Amazon.com) and \(X\) a vectors of covariates

Relationship between \(Y\) and \(D\) is confounded; possibly by high-dimensional variables

Example from Chapter 0 in Applied Causal Inference Powered by ML and AI

Example: price elasticity

- Partially linear model (PLM): \[\begin{align*} Y = \theta_0 D + g(W) + \varepsilon, \quad E[\varepsilon \mid D, W] = 0 \end{align*}\]

- Hierarchy of increasingly complex models yield confidence interval for \(\theta_0\):

- Simple OLS: \((−0.008, 0.050)\)

- OLS with \(243\) controls: \((−0.026, 0.036)\)

- (Double) Lasso with \(p > n\): \((−0.10, −0.029)\)

- DML with GBM: \((-0.139, −0.074)\)

- DML with Transformer: \((−0.21, −0.13)\)

- More predictive methods better able to account and correct for the confounding effects that biased the estimates upward

- Using AI to account for rich text data counteracts confounding effects the most